Salesforce's AI Gamble: Stock Down 45-50% Amidst "Seat Compression"

Alexander Shlimakov specializes in Salesforce, Tableau, Mulesoft, and Slack consulting for enterprise clients across the CIS region. With a proven track record in technical sales leadership and a results-oriented approach, he focuses on the financial services, high-tech, and pharma/CPG segments. Known for his out-of-the-box thinking and strong presentation skills, he brings extensive experience in solution sales and business development.

Salesforce's new AI-powered Slackbot aims to redefine enterprise work, but faces market skepticism and 'seat compression' fears.

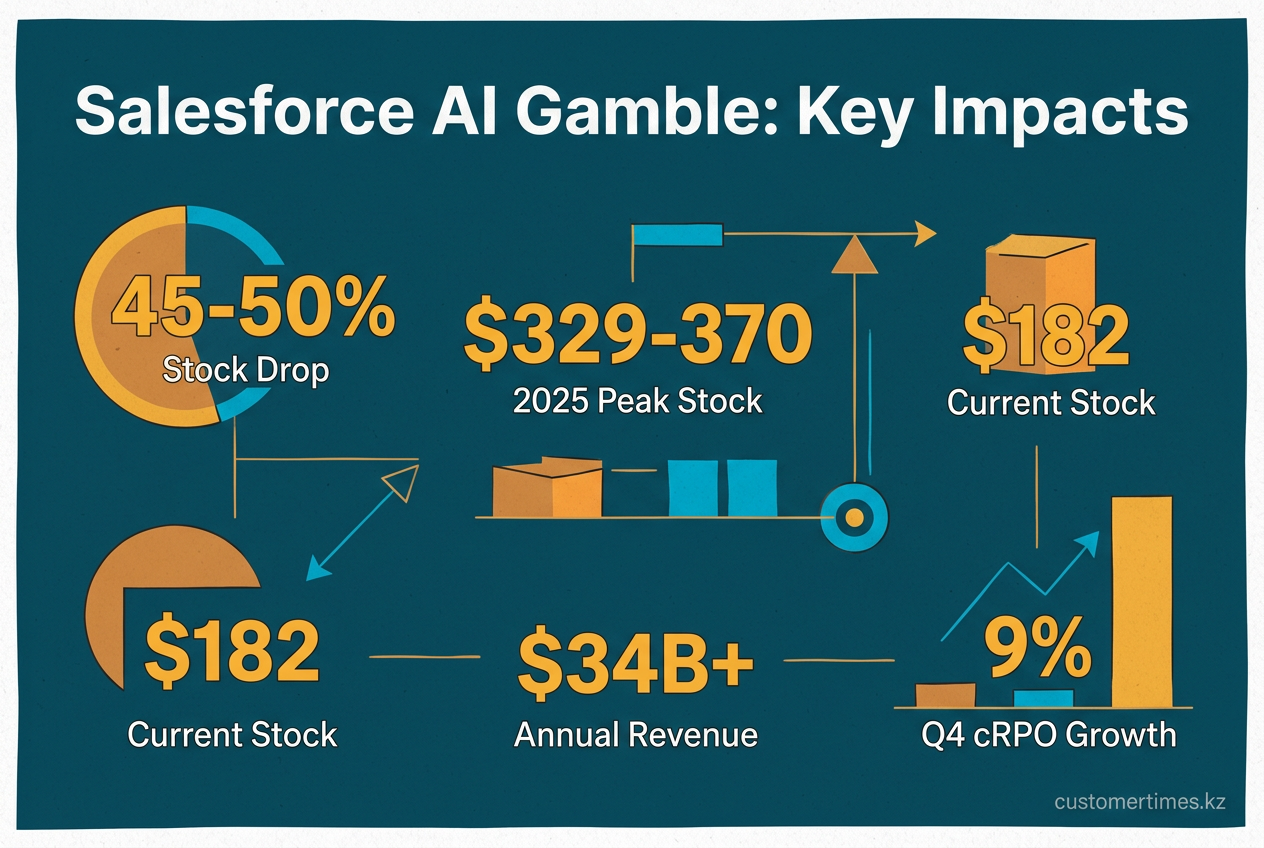

Salesforce's AI gamble on a new agentic operating system has investors fearing 'seat compression,' causing its stock to fall 45-50%. Announced on 1 April 2026 alongside a 41.18 million USD S-8 shelf registration, the AI threatens the company's core per-seat license revenue. In response, Salesforce is aggressively repositioning its upgraded Slackbot as the central tool for enterprise work. While the company aims for growth, the future remains uncertain if AI agents cannibalize its primary revenue source.

What is the impact of Salesforce's AI-powered agentic operating system on its business model?

Salesforce's launch of an AI-powered agentic operating system designed to automate complex office tasks has raised significant investor concern about the erosion of its core revenue stream, a phenomenon known as "seat compression." The technology, which can create AI co-workers and manage tasks across platforms, was unveiled as part of the most aggressive overhaul of Slack since its 27.7 billion USD acquisition.

Initial market reaction was muted, but by mid-April, Salesforce stock was trading near 182 USD, a steep 45-50% decline from its 2025 peak of 329-370 USD. The broader iShares software ETF also posted its worst quarter since 2008. The central question for investors is no longer if AI will boost growth, but if autonomous agents will ultimately erase Salesforce's traditional subscription revenue.

Salesforce's AI-powered agentic operating system introduces significant risk by automating tasks previously done by human users. This could lead to 'seat compression,' where companies purchase fewer software licenses, directly threatening Salesforce's primary subscription-based revenue stream and creating uncertainty about its long-term growth model.

The maths of seat compression

The majority of Salesforce's 34-billion-plus USD in annual revenue is derived from its per-seat subscription model. "Seat compression" describes the direct financial threat posed by AI agents that can perform tasks - like scanning emails or updating sales opportunities - without human intervention, thus reducing the need for licensed seats.

Analyst Nehal Chokshi at Northland crystallized this fear, cutting his price target to 229 USD after fourth-quarter cRPO growth fell to 9%, missing the 10-12% minimum expected by Wall Street.

"If an agent can do the work of three SDRs, you don't buy three licences any more - you buy one orchestration layer and pocket the savings."

- Sell-side note circulating in early April

Slackbot as the new counter-offensive

Salesforce's answer to this existential threat is a strategic counter-offensive to establish Slackbot as the default front door for all enterprise work. An update on 31 March introduced over thirty new features, turning the chat interface into a universal command center. Starting this summer, CEO Marc Benioff has confirmed that all new Salesforce instances will ship with Slack and AI enabled from day one, effectively bundling the agentic layer with its core CRM products.

| Capability | Metric | Implication |

|---|---|---|

| Desktop agent | Monitors any app | Activity data feeds AI training loops |

| MCP router | 6 000 connectors | Customers can bolt on legacy systems without rip-and-replace |

| Native CRM objects | Auto-created from chat | Captures data that used to stay in email |

| Included pricing | Zero extra for Business+ | Removes procurement friction |

Early traction signals

Leaked internal metrics shared with channel partners reveal why management is confident in this bundling strategy, showing powerful early adoption for its "Agentforce" platform:

- 23,000 customers are already using Agentforce.

- The product generated 800 million USD in Q4 ARR, marking the fastest product ramp in the company's history.

- The platform processed 2.4 billion agentic work units last quarter, a sequential increase of 57%.

- Token consumption, a key indicator of automated task volume, has grown fivefold year-over-year.

The partner wedge

To drive market penetration, Salesforce is strategically using system integrators as a wedge, with partners now leading 70% of all Agentforce implementations. This approach allows Salesforce to expand its footprint rapidly while keeping associated services revenue off its own books. Management has guided partners to pursue 1 billion USD in influenced ACV for fiscal 2027, which implies a 6.19 USD multiplier for every dollar of license revenue. The company's internal sales mantra has shifted from "no software" to:

"We make the agent, you make the workflow"

What could still go wrong

Despite this momentum, Salesforce's position is challenged by intensifying competitive pressure on three fronts:

- AI-native upstarts are offering specialized vertical CRM solutions that bypass traditional configuration.

- Microsoft has integrated its own agent store directly into Office 365, posing a threat of bundling at a comparable cost.

- Customer procurement teams are beginning to push for outcome-based pricing (e.g., pay per converted lead), which would hasten the decline of per-seat licenses.

While Salesforce's 30% free-cash-flow margin and double-digit RPO growth provide a cushion for experimentation, any evidence that agent adoption is cannibalising core license revenue could spark another sell-off.

April shelf filing in context

Viewed in this context, the 41 million USD equity shelf filing from April offers a subtle signal of leadership's confidence. Though minor compared to the 25 billion USD accelerated buyback announced in March, it indicates Salesforce intends to continue using stock to reward employees. Companies anticipating a structural decline in revenue often switch compensation to cash. This move suggests that leadership believes its AI pivot will ultimately expand, not shrink, its total addressable market.

Whether that conviction holds through the next two earnings calls will determine if Salesforce is re-evaluated as a growth leader or becomes a cautionary tale of innovation eating its own business model.