Kazakhstan: 88.6% Digital Payments in March 2026, Nearing Cashless Goal

Alexander Shlimakov specializes in Salesforce, Tableau, Mulesoft, and Slack consulting for enterprise clients across the CIS region. With a proven track record in technical sales leadership and a results-oriented approach, he focuses on the financial services, high-tech, and pharma/CPG segments. Known for his out-of-the-box thinking and strong presentation skills, he brings extensive experience in solution sales and business development.

Kazakhstan's payment revolution: 88.6% of transactions are digital, driven by QR codes, instant transfers, and new banking laws.

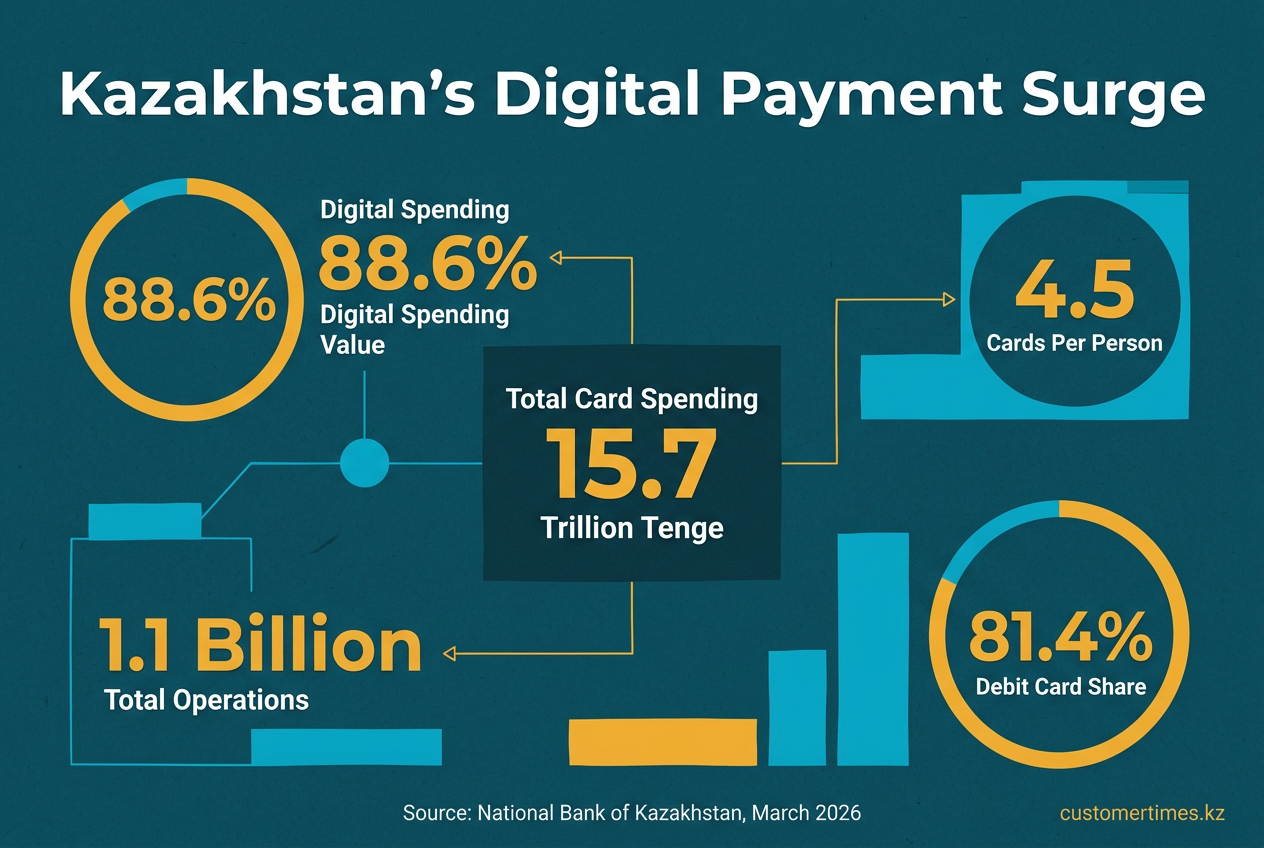

In Kazakhstan, 88.6% of card spending value was digital in March 2026, putting the nation near its cashless goal. Bank cards have evolved from cash substitutes to the primary infrastructure of the economy. High adoption of QR codes, instant transfers, and biometric authentication has made digital payments the standard. With over four bank cards per person, cash usage is diminishing, allowing businesses to save on costs and improve efficiency. Widespread smartphone ownership and internet access are key factors as Kazakhstan aims to make nearly all retail transactions cashless by 2026.

How has Kazakhstan's payment landscape shifted toward digital transactions?

Kazakhstan's payment landscape has rapidly digitized due to key drivers like QR payments, instant transfers, and biometric onboarding. These innovations, supported by regulatory reforms promoting a cashless economy, resulted in 88.6% of card spending value occurring via internet and mobile banking by March 2026.

In March 2026, the National Bank of Kazakhstan recorded a record 15.7 trillion tenge in card spending across 1.1 billion operations. The defining feature of this volume is its digital nature: 88.6% of the value and 78.7% of all transactions were conducted through internet and mobile banking, bypassing physical point-of-sale (POS) terminals.

| Metric | Mar 2026 | Share |

|---|---|---|

| Total transactions | 1.1 bln | 100 % |

| Internet & mobile | 865 mln | 78.7 % |

| POS terminal | 235 mln | 21.3 % |

| Total value | 15.7 trn tenge | 100 % |

| Internet & mobile | 13.9 trn tenge | 88.6 % |

This trend is structural. Data from a year prior shows a similarly high digital share, confirming a sustained shift away from physical payments.

"The majority of cashless transactions were conducted via internet and mobile banking, accounting for 79.7 % of the total number of transactions and 89.8 % of the total transaction volume."

- Hronika.kz, Feb 2026

As of February 2026, Kazakhstan's population held 85.1 million cards, averaging 4.5 per citizen. Debit cards dominate the market, accounting for 81.4% of the total. Credit cards constitute only 15.6%, reflecting a regulatory environment that favors instant debit payments over revolving credit.

What is driving the tap-and-go culture?

-

QR-code rails: A unified interbank QR standard launched in 2025 allows any banking app to scan a single code. Within six months, QR payments became the preferred method for small-value purchases at retailers and gas stations.

-

Instant transfers: The National Bank's real-time payment system processes peer-to-peer and consumer-to-business payments in seconds at no cost. In the first half of 2025, daily traffic grew 34% year-over-year to an average of 6.3 trillion tenge.

-

Biometric onboarding: Remote Know Your Customer (KYC) processes using facial recognition surged by 60% in 2025. This technology enables customers to open a full-service bank account in under three minutes without visiting a branch.

-

Merchant economics: While a traditional POS terminal can cost a small business 15,000-20,000 tenge per month, a static QR code sticker is free, making digital adoption an easy financial decision for micro-merchants.

Regulatory catalysts

A new Banking Law enacted on 25 December 2025 modernized the country's financial regulations, making digital finance a core component of a banking license. The law empowers banks to integrate directly with the National Digital Financial Infrastructure, a unified switch for QR, instant transfers, and central bank digital currency (CBDC) settlement.

"Banks can open digital tenge accounts, issue digital financial assets including stable-coins, converging digital and traditional banking."

- Baker McKenzie, Jan 2026

The reform also introduced consumer protections, such as eliminating penalties for early loan repayment and requiring biometric ID for online credit, ensuring the rapid digital expansion remains secure.

Market impact in numbers

-

Cash-withdrawal share of total card turnover has plummeted from over 50% in 2019 to just 11% by March 2026.

-

Non-bank payment organizations grew by 22% in H1 2025, processing 4.6 trillion tenge and demonstrating that innovation is thriving beyond the established systemic banks.

-

The Digital Tenge pilot had issued 336.6 billion tenge by early 2026 for use cases like budget transfers and SME lending, signaling the CBDC's planned role as a practical, everyday tool.

What businesses feel on the ground

The shift to digital payments delivers tangible benefits for businesses. Retail chains report that cashless transactions reduce queue times by 15-20% and increase average basket values by 7-9%, as customers are not constrained by the cash they carry.

Telecom operators saved an estimated $1.2 million annually in cash-handling costs by moving bill payments to in-app card systems. The trend has even reached traditional markets like Almaty's Barakholka, where vendors using QR codes saw cash withdrawals at nearby ATMs drop 38% in a single quarter.

Looking ahead

The national program "Digital Kazakhstan 2026" aims for 95% of retail turnover to be cashless by the end of that year. With smartphones in over 90% of the population's hands and household fiber optic coverage exceeding 80%, the necessary infrastructure is in place. The main remaining hurdle is behavioral, particularly among older generations. However, with March's 88.6% digital share just 6.4 percentage points from the target, the gap is closing fast.

For banks, the next challenge is monetization. With interchange fees capped, future revenue will depend on value-added services like data-driven credit, investment cross-selling, and merchant analytics. Many are already developing these offerings on powerful Salesforce-based CRM suites. While physical cards may eventually vanish into digital wallets, the 15.7 trillion tenge processed in one month confirms Kazakhstan's payment revolution has passed its tipping point and continues to accelerate.