Cloud Infrastructure Market Soars: AI, IoT Fuel 23.9% CAGR

Cloud infrastructure is booming, driven by AI, IoT, & cybersecurity. Learn about market size, demand, key players, & future trends.

The global cloud infrastructure market is experiencing unprecedented growth, fueled by the accelerating adoption of AI, the Internet of Things (IoT), and advanced cybersecurity solutions. Major enterprises and critical sectors like healthcare are migrating core operations to the cloud to manage vast data sets with greater speed and security. In response, technology leaders such as Amazon, Microsoft, and Google are aggressively expanding their global data center footprints. As data sovereignty rules and demand for specialized hardware increase, the cloud's central role in the digital economy continues to solidify.

What is driving the rapid growth of the global cloud infrastructure market?

The rapid expansion of the global cloud infrastructure market is primarily driven by the increasing adoption of AI, IoT, and cybersecurity. These technologies demand scalable computing, storage, and networking resources, accelerating the move toward hybrid and multi-cloud environments. Key industries like healthcare and evolving regional compliance laws further propel this growth.

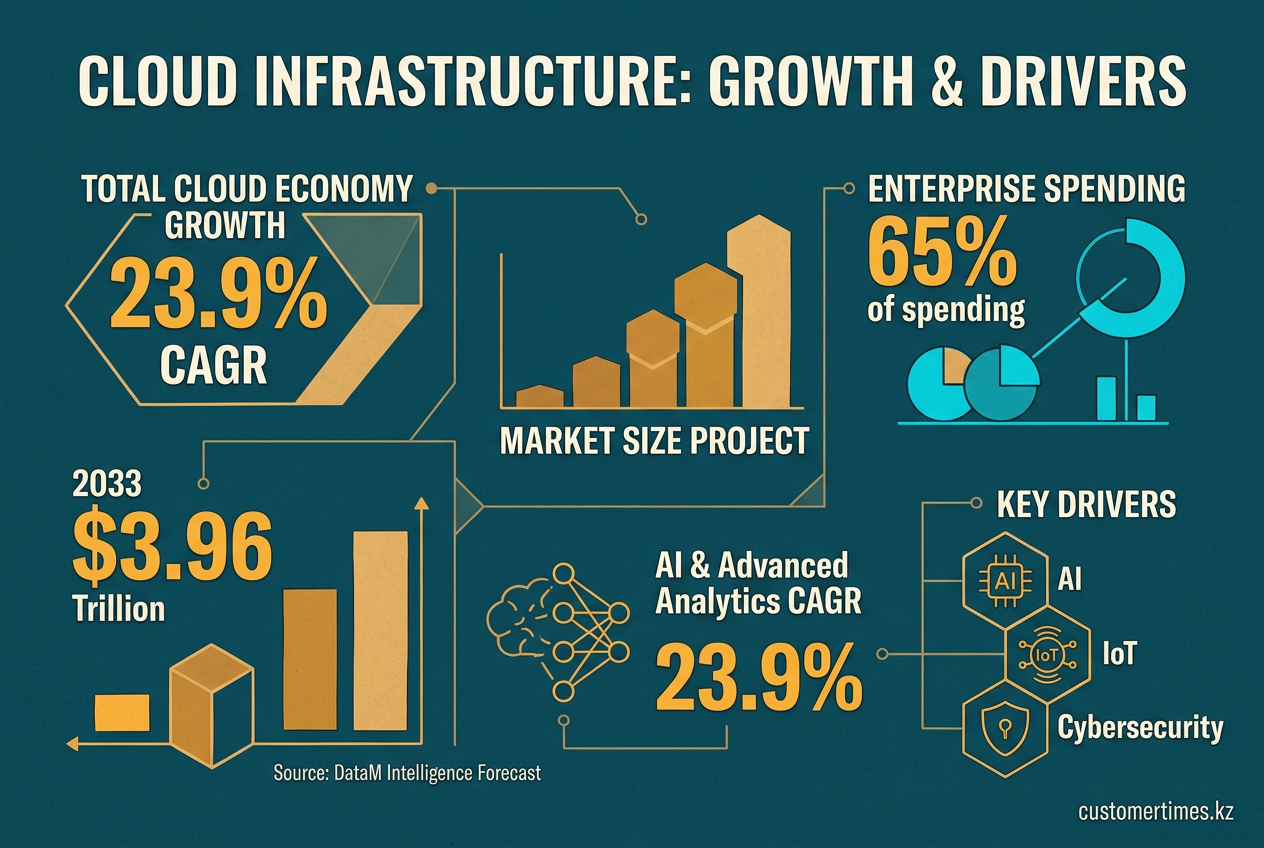

This 'cloud-first' approach is now standard across industries, from hospital imaging in Seoul to logistics in Almaty. Every new application - be it an AI diagnostic tool, a sensor network for fleet management, or a zero-trust security protocol - is predominantly deployed in the cloud. New forecast data by DataM Intelligence confirms this trend, showing that the underlying cloud infrastructure sector - comprising compute, storage, and networking - is on a steep growth trajectory expected to continue through at least 2033.

1. Market size and trajectory

The market's rapid expansion is driven by technologies like AI and IoT that legacy data centers cannot support efficiently. Enterprises are adopting hybrid and multi-cloud strategies to access scalable, on-demand compute and storage, treating infrastructure capacity as a flexible utility to meet evolving business needs.

The total cloud economy, including SaaS, PaaS, and IaaS, is projected to grow from USD 711.6 billion this year to USD 3.96 trillion by 2033, representing a 23.9% compound annual growth rate (CAGR). Within this ecosystem, the cloud infrastructure layer is the fastest-growing substratum. This growth is fueled by demand for AI, IoT, and cybersecurity that exceeds the capabilities of traditional data centers. Hybrid and multi-cloud models have become the standard, with 65% of spending originating from large enterprises that manage capacity as a variable commodity.

2. Demand levers: why buyers keep adding servers that they will never physically see

| Technology | 2025-33 market CAGR | Key Infrastructure Drivers |

|---|---|---|

| AI & advanced analytics | 23.9 % (AI data-centre sub-segment) | GPU/TPU clusters, high-bandwidth memory, low-latency RDMA networks |

| IoT & edge streaming | 18 % (cloud-based IoT solutions) | Regional micro-clouds, MQTT brokers, serverless ingest functions |

| Cyber-security & compliance | 33.6 % (Gen-AI security tools) | Confidential-computing enclaves, key-management HSMs, log-lake storage |

"Capacity is selling as quickly as we can bring it online" - hyperscale operator quoted after announcing one-million-GPU roll-outs for 2026.

3. Competitive heat map

While Amazon Web Services, Microsoft Azure, and Google Cloud dominate the market, competition is intensifying through strategic specialization:

- AWS - added 1.3 GW of power optimized for AI to support U.S. government workloads and plans to deploy over one million NVIDIA Blackwell/Rubin GPUs in new regions from 2026.

- Microsoft - is delivering security-cleared Azure regions tailored for SAP, healthcare, and finance, promoting a "confidential multi-cloud" model for regulated industries.

- Google - is using its proprietary TPU v5 pods to offer AI model training with sub-hour billing granularity, directly competing with AWS's per-second pricing models.

4. Sector spotlight: healthcare and life sciences

In 2025, healthcare accounted for 12% of global cloud spend, and analysts project it will be the most profitable vertical through 2033. Hospital systems are moving large-scale picture archiving and communication systems (PACS) to cloud object storage. Meanwhile, pharmaceutical companies are streaming real-world evidence from IoT-enabled devices directly into cloud-based analytical environments. Illustrating this trend, a regional system integrator in Central Asia migrated a pharmaceutical distributor from a legacy CRM to a cloud-native platform in less than a year. This transition eliminated batch processing downtime and reduced software release cycles from months to days, showcasing the agility now expected by businesses.

5. Regional snapshots

Growth patterns vary by region, with the Asia-Pacific market poised for the most significant expansion.

| Region | 2025 share | 2033 outlook | Growth catalysts |

|---|---|---|---|

| Americas | 38 % | Steady | AI arms race, federal compliance mandates |

| EMEA | 30 % | +2 pts | Green data-center regulations driving retrofits |

| Asia-Pacific | 32 % | +4 pts | 5G roll-outs, smart-city budgets, sovereign-cloud policies |

Kazakhstan exemplifies the Asia-Pacific trend. Its data residency laws mandate that personal data and encryption keys remain within the country. Cloud providers address this by establishing "in-country regions" that connect to global networks, allowing multinational corporations to use a single, worldwide codebase while ensuring local compliance.

6. Capital intensity: record-breaking build-outs

In February 2026, Amazon announced a landmark USD 200 billion capital expenditure plan for the year, far surpassing previous investment cycles. Approximately USD 50 billion of this is allocated for U.S. federal government workloads, indicating that government agencies are becoming major anchor tenants for cloud services. This expansion was supported by a subsequent USD 42 billion bond issuance, which was readily underwritten, demonstrating strong investor confidence in long-term cloud capacity investments despite potential short-term impacts on margins.

From software-led growth we have moved to an infrastructure-led era where gigawatts, not features, decide market share.

7. What buyers should watch

Organizations investing in cloud infrastructure should monitor several key factors:

- Power & water: AI clusters require 50 - 70 kW of power per rack, making renewable energy access and liquid-cooling infrastructure critical factors in data center site selection.

- Chip substitution: Using specialized processors like AWS Trainium2 and Google TPU v5 can lower AI training costs per parameter by 30 - 40% compared to general-purpose GPUs, but this may necessitate rewriting software frameworks.

- Lock-in vs. portability: While new open-source tools like Kubernetes and Crossplane promise to abstract vendor-specific APIs, access to GPU quotas often remains a powerful negotiating tool for providers, creating potential lock-in.

- Security SLA drift: With generative AI-powered cyber threats growing 33% annually, service level agreements (SLAs) for incident response times must shift from hours to minutes to be effective.

8. Adjacent markets pulled along

The growth in cloud infrastructure is also driving significant expansion in related markets:

- The data center cooling market is expected to grow from USD 16.4 billion in 2025 to USD 45.8 billion by 2033 (a 13.6% CAGR) as direct-to-chip liquid cooling becomes standard.

- The market for accelerator silicon (GPUs, TPUs, DPUs) is projected to increase nearly eightfold, from USD 21.5 billion to USD 169 billion, during the same period.

The trend is clear: cloud infrastructure forms the fundamental layer for the next wave of technological innovation. Organizations that align their AI, IoT, and security strategies with the hyperscale supply chain today are securing their position on the digital factory floor of the future.